California Underwritten Title Company Bond: A Comprehensive Guide

This guide provides information for insurance agents to help their customers obtain a California Underwritten Title Company bond.

At a Glance:

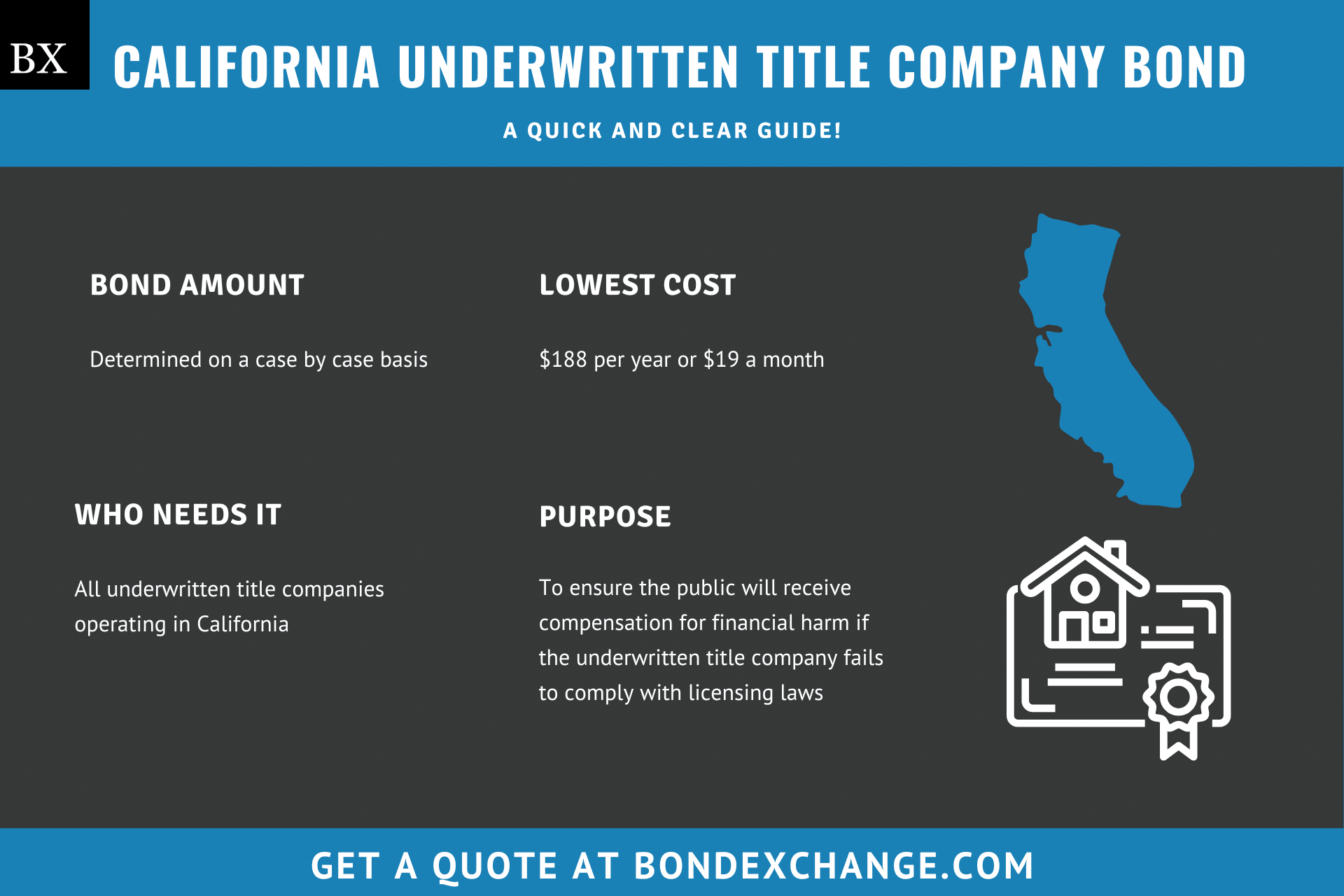

- Lowest Cost: $188 per year or $19 a month

- Bond Amount: Determined on a case-by-case basis (more on this later)

- Who Needs It: All underwritten title companies operating in California

- Purpose: To ensure the public will receive compensation for financial harm if the underwritten title company fails to comply with licensing laws

- Who Regulates Underwritten Title Companies in California: The California Department of Insurance

Background

California Insurance Code 12389 requires all domestic underwritten title companies operating in the state to obtain a license from the Department of Insurance. The California legislature enacted the licensing requirement to ensure underwritten title companies do not engage in unethical business practices. To provide financial security for enforcing licensing laws, underwritten title companies must purchase and maintain a surety bond to be eligible for licensure.

What Is the Purpose of a California Underwritten Title Company Bond?

Underwritten title companies that provide title and escrow services to California residents must purchase a surety bond as part of the application process to obtain a business license. The bond protects the public from losses should the underwritten title company fail to abide by the regulations outlined in California Insurance Code 12389. Specifically, the bond financially protects claimants if the underwritten title company misappropriates funds or commits fraud. In short, the bond is a type of insurance that protects the public if the underwritten title company violates the terms of its license.

How Can an Insurance Agent Obtain a California Underwritten Title Company Bond?

BondExchange makes obtaining an California Underwritten Title Company bond easy. Simply log in to your account and use our keyword search to find the “underwritten title company” bond in our database. Don’t have a login? Gain access now and let us help you satisfy your customers’ needs. Our friendly underwriting staff is available by phone at (800) 438-1162, email, or chat from 7:30 AM to 7:00 PM EST to assist you.

At BondExchange, our 40 years of experience, leading technology, and access to markets ensures that we have the knowledge and resources to provide your clients with fast and friendly service whether obtaining quotes or issuing bonds.

Not an agent? Then let us pair you with one!

![]()

Click the above image to find a BX Agent near you

How Is the Bond Amount Determined?

California Insurance Code 12389 states that the bond amount must be calculated on a case-by-case basis and is based on the aggregate number of documents recorded and filed in the previous calendar year in all counties where the underwritten title company is licensed.

Details on how to calculate the correct limit for the Underwritten Title Company bond and the corresponding net worth requirements can be found in the chart below:

| Number of Documents | Amount of Required Net Worth | Bond Amount Required |

|---|---|---|

| Less than 50,000 | $75,000 | $50,000 |

| 50,001 to 100,000 | $120,000 | $50,000 |

| 100,001 to 500,000 | $200,000 | $100,000 |

| 500,001 to 1,000,000 | $300,000 | $100,000 |

| 1,000,001 or more | $400,000 | $100,000 |

Is a Credit Check Required for the California Underwritten Title Company Bond?

Surety companies will run a credit check on the underwritten title company to determine eligibility and pricing for the California Underwritten Title Company bond. Underwritten title companies with excellent credit and work experience can expect to receive the best rates. Applicants with poor credit may be declined by some surety companies or have to pay higher rates. The credit check is a “soft hit”, meaning that the credit check will not affect the applicant’s credit.

How Much Does the California Underwritten Title Company Bond Cost?

The California Underwritten Title Company bond can cost between 0.5% to 5% of the bond amount per year. Monthly subscription options are also available. Insurance companies determine the rate based on several factors including your customer’s credit score and experience. The chart below briefly references the approximate bond cost on the $50,000 bond requirement.

$50,000 Underwritten Title Company Bond Cost

| Credit Score* | Bond Cost (1 Year) | Bond Cost (1 month) |

|---|---|---|

| 720+ | $188 | $19 |

| 680 – 719 | $225 | $23 |

| 660 – 679 | $350 | $35 |

| 649 – 659 | $500 | $50 |

| 629 – 648 | $750 | $75 |

| 600 – 628 | $1,250 | $125 |

| 580 – 599 | $1,750 | $175 |

| 550 – 579 | $2,000 | $200 |

| 525 – 549 | $2,500 | $250 |

| 500 – 524 | $3,000 | $300 |

*The credit score ranges do not include other factors that may result in a change to the annual premium offered to your customers, including but not limited to, years of experience and underlying credit factors contained within the business owner’s credit report.

How Does California Define “Underwritten Title Company”?

To paraphrase California Insurance Code 12340.5, an underwritten title company is a business that prepares title searches, title examinations, title reports, title certificates, and/or abstracts of titles for a title policy.

Underwritten title companies should not be confused with “title insurers” as they do not actually issue title insurance policies. Title insurers act as a guarantor of title insurance policies and are exempt from this specific surety bond requirement.

BondExchange now offers monthly pay-as-you-go subscriptions for surety bonds. Your customers are able to purchase their bonds on a monthly basis and cancel them anytime. Learn more here.

How Do Underwritten Title Companies Apply for a License in California?

Underwritten title companies in California must navigate several steps to obtain a license. Below are the general guidelines, but applicants should refer to the Department of Insurance’s application webpage for specific details on the process and access to all necessary forms.

License Period – The California Title Company License does not expire and is issued for an indefinite term (annual renewal fees still apply).

Step 1 – Purchase a Surety Bond

Underwritten title companies operating must purchase and maintain a surety bond (limits outlined above).

Step 2 – Meet the Qualifications

The Department of Insurance will issue a license after considering the following:

- Minimum net worth and working capital of the applicant

- Reasonableness of the applicant’s plan of operation

- Lawfulness and quality of the applicant’s investments

- Financial stability of the applicant

- Competency, character, and integrity of the applicant’s management

- Ownership and control of the applicant’s issued and outstanding shares

- Fairness and honesty of the applicant’s methods of doing business

- Method by which the applicant was promoted if any of its promoters remain as stockholders or in management

- Possible hazard to the public

Step 3 – Submit Completed Documents and Pay Fees

When applying for a license, the applicant must provide the Department with the information and documentation requested in the application, including all supplemental information requested during the course of the review. The appropriate forms and applicable fees are listed below:

- Application for License to Act as an Underwritten Title Company webpage

- Securities Forms and Instructions

- Authorization for Disclosure of Financial Records to the California Insurance Commissioner

- A filing fee of $849

If the underwritten title company is seeking to extend its license to an additional county, an extra fee of $494 is required per county.

How Do California Underwritten Title Companies Renew Their License?

According to the California Department of Insurance, underwritten title companies are required to submit a license renewal fee of $567 each year. The Department should send a notice for renewal to the licensee in advance of the due date.

What Are the Insurance Requirements for Underwritten Title Companies in California?

According to California Insurance Code 12389.6, the underwritten title company must purchase and maintain a fidelity bond or insurance policy that is satisfactory to the Department of Insurance. The fidelity bond or insurance policy must cover losses caused by misappropriation, disappearance, or other wrongful use of escrow funds deposited with the underwritten title company.

How Do California Underwritten Title Companies File Their Bonds?

Underwritten title companies should submit their completed bond forms, including the power of attorney when submitting their license applications to the California Department of Insurance (see mailing address listed below).

Department of Insurance

Corporate Affairs Bureau

1901 Harrison Street, 6th Floor

Oakland, CA 94612

The surety bond requires signatures from the surety company, as well as a representative from the underwritten title company. The surety company should include the following information on the bond form:

- The legal name of the individual buying the bond

- Surety company’s name

- Date the bond is signed

What Can California Underwritten Title Companies Do to Avoid a Claim Against Their Surety Bond?

The best way to avoid a bond claim as an underwritten title company is to simply comply with state license laws. This includes applying all funds received honestly, as well as properly performing each escrow obligation. For example, failure to maintain a record of all receipts and disbursements of escrow funds can lead to a bond claim for negligence.

What Other Insurance Products Can Agents Offer Underwritten Title Companies in California?

In addition to their business license bond, California requires underwritten title companies to obtain either a fidelity bond or other insurance coverage. Contact BondExchange to obtain a fidelity bond.

How Can Insurance Agents Prospect for California Underwritten Title Company Customers?

California conveniently provides a public database to search for active underwritten title companies in the state. The database can be accessed here. Contact BondExchange for additional marketing resources. Agents can also leverage our print-mail relationships for discounted mailing services.