Do Surety Companies Offer Refunds?

Insurance agents often ask us “are premiums on surety bonds refundable?” There are multiple factors at play when determining your customer’s refund eligibility. Generally speaking, the surety company will asses the following when determining if they can return premium:

- Does their rate filing allow for return premium?

- Can the bond be cancelled?

- What portion of the bond term is “earned” vs “unearned”?

In this week’s blog post, we break down surety company requirements for returning premium, and provide insurance agents with the information needed to properly communicate the rules to their clients.

Why Would Your Customer Need a Refund on Their Surety Bond?

If your customer is seeking a refund for any premium paid on a surety bond, it is most likely for one of the following reasons:

- Purchased a surety bond only to later find out the bond is not required

- Purchased a surety bond only to be denied a business license or permit

- Purchased a surety bond and then decided not to obtain the business license or permit or went out of business

- Purchased the wrong surety bond

- Paid for a multi year term and, prior to the term expiration, the bond is no longer needed.

Regardless of the reason, your customer is going to be expecting some form of refund if their bond needs to be cancelled mid-term. Navigating the specifics of a surety company’s policy on returning premium can be arduous, but we’ve broken down the basics for you in the following sections.

When Do Surety Companies Refund Premium?

Surety companies view premiums as payment for their assumption of the risk listed in the bond agreement, so as long as the bond can be cancelled and the surety has a way to extinguish their liability under the bond, they should refund any premium paid, but not earned.

When a bond is cancelled mid-term, the surety company should pro-rate the premium based on the premium that has been earned on the bond. In general, surety companies calculate the earned premium on a daily basis. For example, if a bond is issued for a 1 year term starting on January 1, 2021, on January 31, 2021, the surety company will have earned 31 days of the bond premium. In addition, most surety bonds contain a cancellation provision (usually between 30-60 days) that extends the surety companies liability by that period. So for our example above, a bond with a 30 day cancellation period would have 31 days of earned premium, plus the 30 day cancellation period, for a total of 61 days of earned premium.

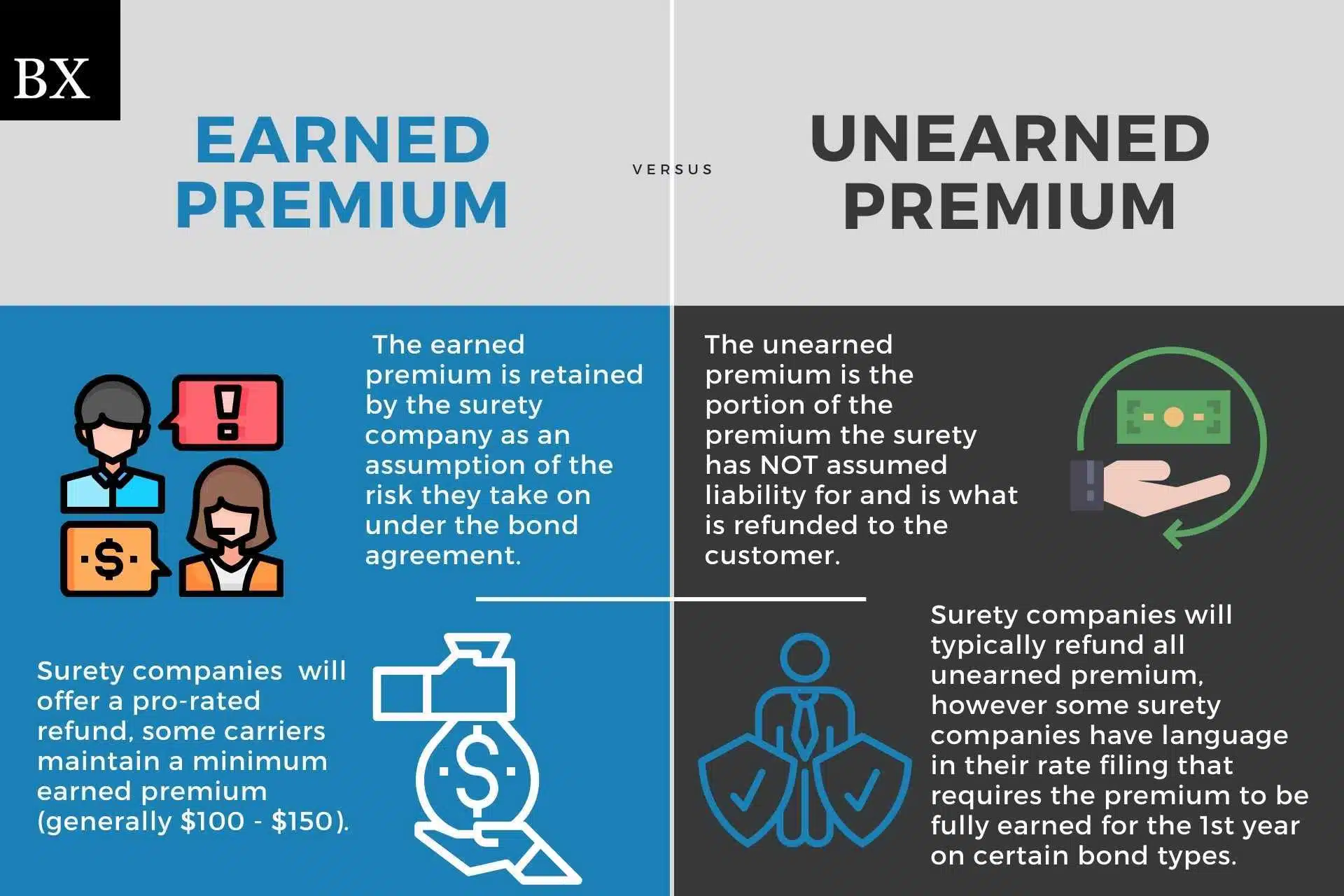

The earned premium is retained by the surety company as an assumption of the risk they take on under the bond agreement. The unearned premium is the portion of the premium the surety has not yet assumed liability for and is what is refunded to the customer.

If a surety company pays out a bond claim, the bond’s indemnity agreement holds the principal legally responsible for repaying the surety company for all claims handling expenses. Most carriers will hold the return premium as collateral on bonds that are cancelled due to claims being filed against it.

It is worth noting that while most carriers will offer a pro-rated refund, some carriers maintain a minimum earned premium (generally $100). The purpose for the minimum earned is to compensate the surety company for the costs incurred in issuing the surety bond. Therefore, if your customer’s bond premium is less than $100, it’s possible there wouldn’t be any return premium available even if it’s cancelled mid-term.

Although many surety companies will return unearned premium, many surety brokers do not refund premiums. These unscrupulous brokers may include language in their bond agreements that gives them the ability to keep these refunds, so we suggest to read the bond agreements carefully. At BondExchange, we always refund unearned premium, and we leverage our size and strong carrier relationships to secure refunds for your customers whenever possible. We are also able to offer payment plans on bonds with premiums exceeding $500 with no interest to your customers.

Are There Any Situations When Premium Would not be Refunded?

Surety companies will typically refund all unearned premium, however there are two distinct situations that will cause a bond to be ineligible for a refund:

- If the bond does not have a cancellation clause, therefore it cannot be cancelled mid-term and will have no unearned premium

- If a surety company chooses to add language to their rate filing excluding refunds on certain bond types and situations.

For example, probate, performance/payment, and freight broker bonds have specific reasons as to why the first year’s premium is fully earned at issuance:

- Probate bonds require a release from the court requiring them to release the liability of the surety. In these situations, the surety considers the first year’s premium fully earned, but will return premium on renewal or multi-year terms

- Performance/Payment bonds provide a project owner with a guarantee that work will be completed as specified in the contract. The time frame individual projects can vary and because the surety is on the hook for the duration of the project, the premium for performance/payment bonds is fully earned once the bond is issued. Should the project cost come in a lower amount, the surety can refund premium through a process known as an underrun

- Freight Broker bonds are a more hazardous class of business and due to the frequency of claims and administrative expense with filing the bonds, surety companies consider premiums to be fully earned at issuance. Most carriers have this provision built into their rate filings.

At BondExchange, we have been able to negotiate with some carriers to allow for refunded premium and we fight for carriers to return premium at cancellation.

If the surety (or broker) can obtain the original bond and confirm it was not filed with the obligee the bond can be flat cancelled resulting in a full refund to your customer. Generally, it is much easier to accomplish this if the surety or broker is notified as soon as the issue is discovered. It is important to consult with surety experts prior to purchasing a bond to ensure your customer is purchasing exactly what they need.

How Can an Insurance Agent Obtain a Surety Bond?

BondExchange makes obtaining a surety bond easy. Our thoroughly developed online system was built for insurance agents like you. Simply login to your account and use our keyword search to find your bond in our database. Don’t have a login? Gain access now and let us help you satisfy your customers’ needs. Our friendly underwriting staff is available by phone (800) 438-1162, email or chat from 7:30 AM to 7:00 PM EST to assist you.

Not an agent? Then let us pair you with one!

![]()

Click the above image to find a BX Agent near you

As a longtime professional in the Insurance Premium Finance industry, I am oftentimes asked by our independent insurance agents to provide financing for surety bonds either separately or in conjunction with a property and casualty policy. As you are probably aware, the terms and conditions in our finance agreement grant us the ability to cancel, therefore providing the collateral necessary to finance the loan. I would love to be able to accommodate these clients, giving them an alternative to pay for the bond in full. Is there any consideration to provide the finance company the ability to cancel the bond in the event of non-payment? Even a reasonable minimum earned premium provision would help offset a potential loss. Then an informed credit decision could be made, giving the consumer alternative payment options.

Thank You

Thank you for your question! We allow third party financing from our agents; however, most of our agents prefer to utilize our own in-house no interest monthly payment option that we offer on all cancellable bonds at or over a $500 premium.

We have found there is little need for a 3rd party financing company to be involved given our in house payment plan option.

Let us know if you have any other questions.